Are you involved in Riba unknowingly?

Riba, or interest, is a practice that has economic, spiritual and moral consequences. What considered has ‘growth’, now it begs the question if ‘growth’ means to exploit, increase inequality and create injustice? Hence why, Islam forbids it.

But what exactly is Riba, why is it haram, and how are you entangled in it without realizing it?

Why is Riba haram in Islam?

Riba refers to the interest or profit gained from typically from loans where one party benefits at the expense of another. The Quran has mention multiple times with clear warning about its negative impacts.

Surah Al-E-Imran (3:130):

يَـٰٓأَيُّهَا ٱلَّذِينَ ءَامَنُوا۟ لَا تَأْكُلُوا۟ ٱلرِّبَوٰٓا۟ أَضْعَـٰفًۭا مُّضَـٰعَفَةًۭ ۖ وَٱتَّقُوا۟ ٱللَّهَ لَعَلَّكُمْ تُفْلِحُونَ

"O you who have believed, do not consume usury, doubled and multiplied, but fear Allah that you may be successful."

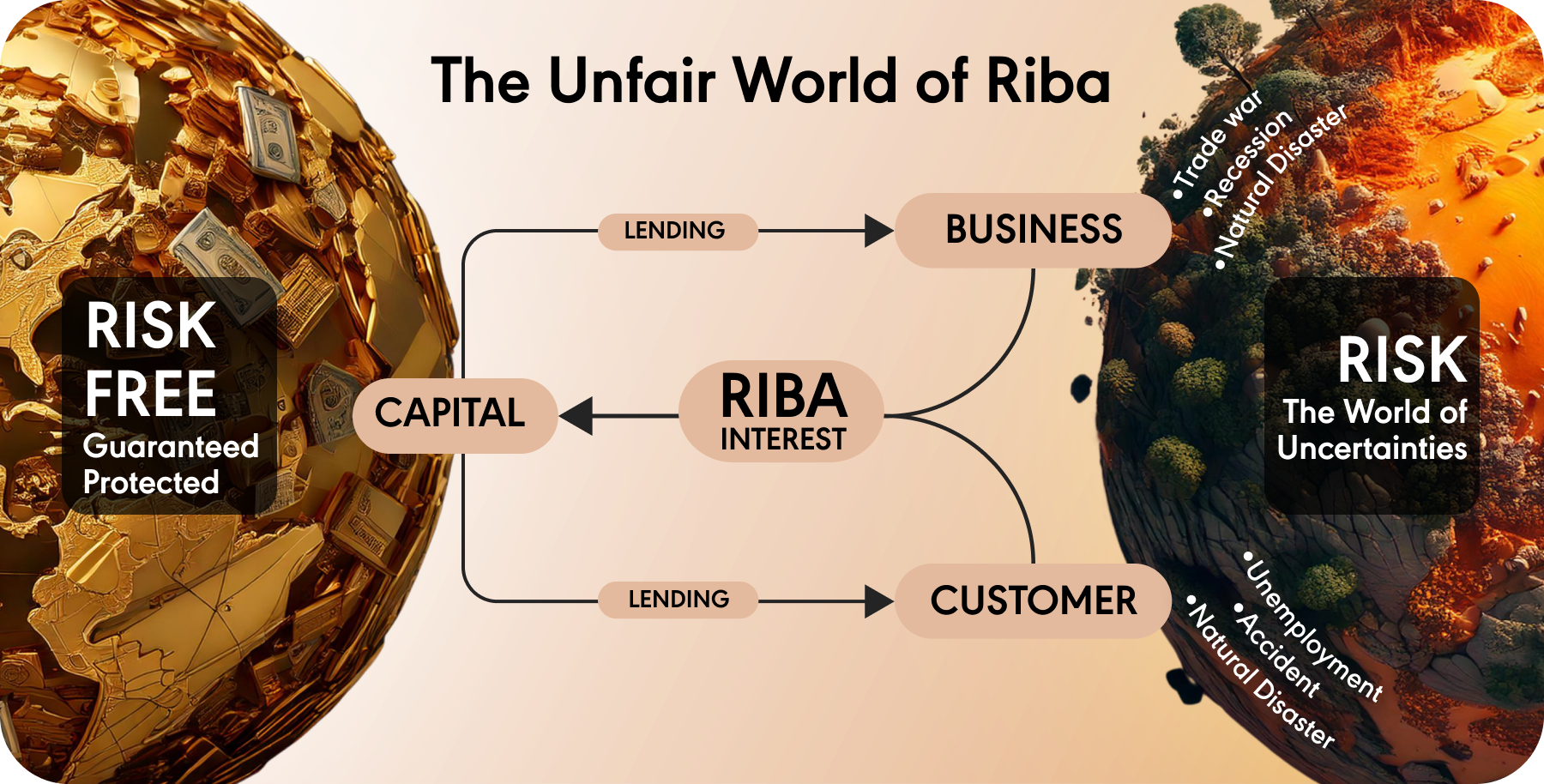

The core issue with riba is that it creates an unjust system where wealth is accumulated not through effort or productivity but by means of extracting and exploiting those in need. Capital or wealth in Islam should be distributed and circulated, not hoarded and being protected for the purposes of greed.

It puts the borrower at a disadvantage, trapping them in a cycle of debt while the lender enjoys guaranteed profits without sharing any of the risks.

This imbalance is seen as one of the root cause of injustices in Islam. The Prophet Muhammad (peace be upon him) emphasized the dangers of riba, not just as a financial issue but as a spiritual one. Engaging in riba distances people from the ethical values of fairness, mutual benefit, and compassion, which are central to Islamic teachings.

You may be trapped in Riba unknowingly.

It seems really impossible to escape from the web of Riba which has been rooted in our daily life. Mortgages, car loans, and credit cards are so common that we often use them to manage our lives, hoping they will help us build a more secure future. This makes avoiding riba especially challenging for those who wish to stay true to Islamic principles.

However, awareness is the first step towards change. By understanding what you are involved in, we can start making little changes that align with our beliefs. Let’s look at two common traps:

- Credit Card

The total credit card debt in Malaysian stood at RM 4.52 billion as of October 2024, with approximately 9.92 million credit cards in circulation as of July 2021. This means each credit card carries an average debt of RM455. On a larger scale, 3 out of every 5 Malaysians owns a credit card.

You likely have at least one credit card in your wallet right now. It’s a convenient option for when you need quick access to cash. Some credit cards don’t charge interest if you pay the full balance on time. However, interest is charged on any unpaid balance, and that is riba.

Credit cards can be risky, not only because of riba but also due to the tempting trap of ongoing debt repayments. If you didn’t have enough money to make the purchase upfront, how sure are you could afford it monthly with high-interest rates?

- Buy Now Pay Later (BNPL)

Bank Negara Malaysia stated that 25% of Malaysians allocate 60% of their income solely to repayments.

Today, instalment options for large purchases are widely available, but they almost always come with interest. Whether it's your preferred mobile phone or a piece of furniture you’ve been eyeing, these instalment plans usually involve riba.

- Housing Loans

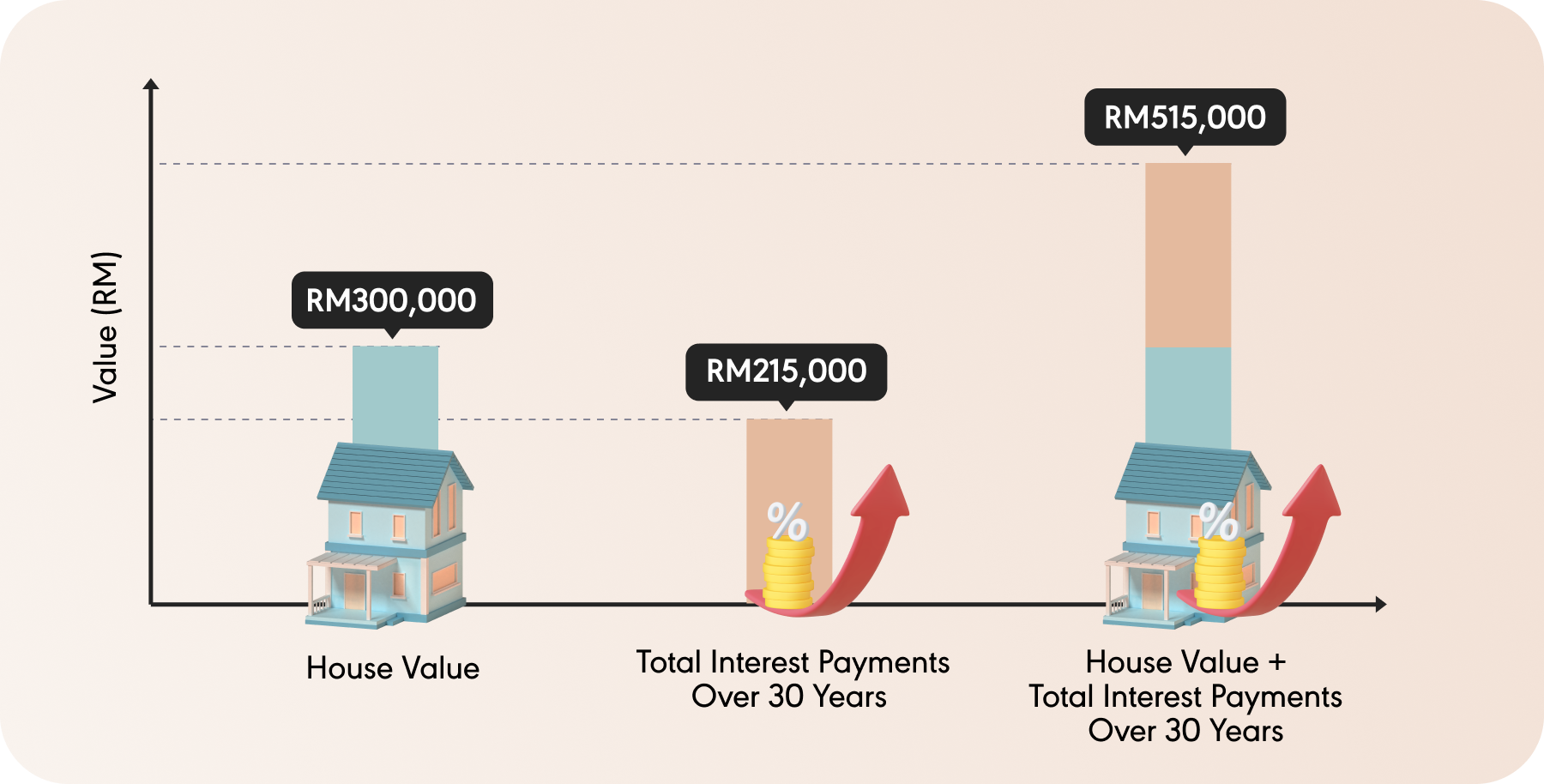

Everyone dreams of owning a home. It’s often seen as a major life milestone and a sign of stability and success. The option to spread payments over many years — often up to 35 years — may initially seem affordable, but it can lead to decades of financial commitment and rising costs due to interest.

To put this into perspective, a 30-year loan at an interest rate of 4% on a property costing RM300,000 results in over RM215,000 in interest alone by the end of the term. This means the borrower ends up paying over RM500,000 for a RM300,000 home.

If your home is financed through an interest-based loan, can it still be truly considered an asset? An asset ideally brings value and financial security, yet with riba-based loans, it can become a long-term liability, with payments consuming a significant portion of your income for decades.

How to spot Riba?

You may be participating with riba unknowingly either as a recipient or contributor to riba. The simplest question you can ask yourself is in the context of money that you would give or take.

When I give money, am I receiving Riba?

For the purposes other than investing, am I getting back with more money than I am giving?

- Guaranteed or Fixed Earnings in Bank Accounts

A bank account that promises a fixed interest or profit rate annually, regardless of economic conditions would mean that the bank is lending your money and sharing the interest charged on the lending with you.

- Interest on Lending Money

If you lend money to a friend or entity and charge a percentage as “interest” on the principal amount, you are receiving Riba, even if agreed upon mutually.

When I take money, am I giving Riba?

Do I have to return more money than what I took?

- Loans

Borrowing money from a bank or institution with an agreed interest rate (e.g. 5% annually) means you’re giving Riba when repaying.

- Instalment Plans with Late Payment Penalties

Some 0% interest instalment plans may penalize late payments with interest charges, turning the agreement into one that involves Riba.

- Credit Card with Interest on Balances

If you carry forward unpaid balances on credit cards, the interest charged on those balances is Riba.

What can you do though?

By this point, you may be asking yourself: what can I do?

Start by minimizing your exposure to riba. If there are other alternatives, consider them. For example, renting could be a better option than purchasing a house with an interest-based housing loan.

When we make these choices, we want to plant a seed of hesitation — a pause. A moment to reflect.

At Wahed, our vision is to create a world free from interest. We believe that growth should come from investing in real assets, where risk and reward are shared equitably — not from interest rates. Not a system where communities are forced to take high-interest loans just to put a roof over their heads.

Join over 400,000 members of the Wahed community in supporting this mission.

It all starts with you.

Risk Warning: Equity investments are not readily realisable and involve risks, including loss of capital, illiquidity, lack of dividends and dilution, and it should be done only as part of a diversified portfolio. Investments of this type are only for investors who understand these risks. You will only be able to invest in the company once you have met our conditions for becoming a registered member.

Please visit www.wahed.com/uk/ventures/risk for our full risk warning.

Risk Warning: As with any investment, a Wahed Invest Ltd investment puts your money at risk, as the value of your investment can go down as well as up. The tax treatment of your investment will depend on your individual circumstances and may change in the future. If you are unsure about whether investing is right for you, please seek expert financial advice.

Please visit www.wahed.com for our full terms and conditions

Maydan Capital Limited, trading as WahedX, is registered in England and Wales (Company No. 13451691), registered office: 87-89 Baker Street, London, W1U 6RJ, UK. Maydan Capital Ltd (FRN: 963613) is an appointed representative of Wahed Invest Ltd (FRN: 833225), an authorised and regulated firm by the Financial Conduct Authority.Wahed Invest Ltd. is registered in England and Wales (Company No. 10829012), registered office: 87-89 Baker Street, London, W1U 6RJ, UK and is authorised and regulated by the Financial Conduct Authority: FRN 833225.

Subscribe For More Islamic Finance Content

As with any investment, a Wahed Invest Ltd investment puts your money at risk, as the value of your investment can go down as well as up. The tax treatment of your investment will depend on your individual circumstances and may change in the future. If you are unsure about whether investing is right for you, please seek expert financial advice.

Wahed Invest LLC (Wahed) is a US Securities and Exchange Commission (SEC) registered investment advisor. Wahed Invest provides brokerage services to its clients through its brokerage partner Apex Clearing Corporation, a member of NYSE - FINRA - SIPC and regulated by the SEC and the Commodity Futures Trading Commission. Registration does not imply a certain level of skill or training. Wahed does not intend to offer or solicit anyone to buy or sell securities in jurisdictions where Wahed is not registered or a region where an investment practice like this would be contrary to the laws or regulations. Any returns generated in the past do not guarantee future returns. All securities involve some risk and may result in loss. Any performance displayed in the advertisements or graphics on this site are for illustrative performances only.

Disclaimer: Wahed Technologies Sdn Bhd ("Wahed") is a Digital Investment Manager (DIM) licensee issued by Securities Commission Malaysia (eCMSL/ A0359/2019). It is part of Wahed Inc. Wahed is authorized to conduct a fund management business that incorporates innovative technologies into automated portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007. All investments involve risks, including the possibility of losing the money you invest, and the track record does not guarantee future performance. The history of returns, expected returns, and probability projections is provided for informational and illustrative purposes, and may not reflect actual future performance. Wahed is not responsible for liability for your trading and investment decisions. It should not be assumed that the methods, techniques, or indicators presented in this product will be profitable, or will not result in losses. The previous results of any trading system published by Wahed, through the Website or otherwise, do not indicate future returns by that system, and do not indicate future returns that will be realized by you.

Wahed Invest Limited is regulated by ADGM’s Financial Services Regulatory Authority (“FSRA”) as an Islamic Financial Business with Financial Services Permission for Shari’a Compliant Regulated Activities of Managing Assets and Arranging Custody [Financial Permission No. 220065]. Our ADGM Registered No. is 000004971.

Wahed assumes no obligation to provide notifications of changes in any factors that could affect the information provided. This information should not be relied upon by the reader as research or investment advice regarding any issuer or security in particular. Any strategies discussed are strictly for illustrative and educational purposes and should not be construed as a recommendation to purchase or sell, or an offer to sell or a solicitation of an offer to buy any security. Furthermore, the information presented may not take into consideration commissions, tax implications, or other transactional costs, which may significantly affect the economic consequences of a given strategy or investment decision. This information is not intended as a recommendation to invest in any particular asset class or strategy or as a promise of future performance.

There is no guarantee that any investment strategy will work under all market conditions or is suitable for all investors. Each investor should evaluate their ability to invest long term, especially during periods of downturn in the market. Investors should not substitute these materials for professional services and should seek advice from an independent advisor before acting on any information presented. Any links to third-party websites are provided strictly as a courtesy. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites. When you access one of these websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites.