Halal IRAs: Pros & Cons

Let’s dive into the world of Halal IRAs*, shall we?

They say that sometimes, the best way to know what to do is to know what not to do. With that being said let's examine what wouldn’t constitute a halal investment in your IRA so that you know what to look out for.

Under the guidance of Shar'iah law, Islamic finance forbids specific financial activities. These include the collection or payment of interest (known as riba), and investments in sectors deemed harmful to society, such as gambling, alcohol, and tobacco, to name just a few. Additionally, Shar'iah law prohibits excessive risk-taking (referred to as gharar), which in many ways can be seen as a form of gambling in the business world.

Now that we have a better understanding of what constitutes a Halal investment, we can move on to understanding the vehicle driving those investments—the Individual Retirement Account (IRA).

Before we dive off the deep end, it's worth taking a step back to address two key questions.

What is an IRA? & Why should I care?

In its simplest form, an IRA is an account that is designed to help you save for your retirement through tax sheltering.

If retirement is your long-term financial goal, the tax benefits of an IRA can significantly accelerate the growth of your investments over time when compared to a standard savings account.

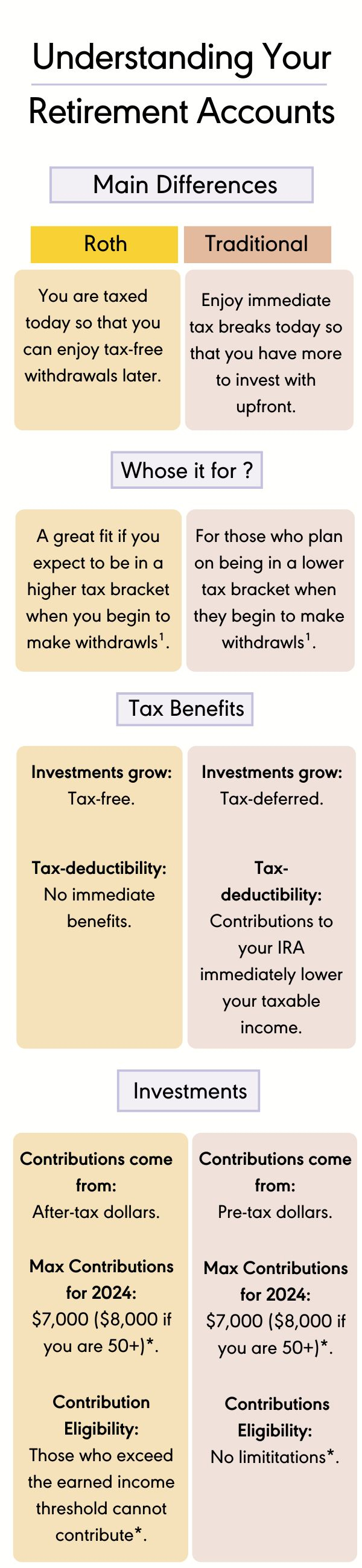

There are many different flavors of IRAs out there, but the two most popular ones—the traditional IRA and Roth IRA—are the ones that we’ll include in our review of the pros and cons of IRAs.

Traditional IRA: With a Traditional IRA, you can enjoy the tax benefits we mentioned earlier right away. When you contribute to your account, it reduces your taxable income for the current year, giving you more money to invest with upfront. The only drawback is that you will be taxed when you withdraw your funds at retirement.

Roth IRA: With a Roth IRA, you pay taxes on your investments now so that they can grow, and when you withdraw the funds at retirement, you do not have to pay any additional taxes.

For our visual learners, we’ve distilled this information into a straightforward and easy-to-digest graphic:

Now that you know a little more about the two accounts we’ve based our analysis on let's take a look at some of the Pros & Cons of investing with an IRA

The Good Stuff about IRAs:

- Tax Advantages: Without a doubt the most significant benefit of using an IRA to fund your retirement are the tax advantages we mentioned above. Another item you’ll want to keep in mind as you’re making deposits are your current and future tax brackets, as strategic planning can make a serious impact on your tax savings.

For example, if you’re a Gen-Z or Millennial who began investing early, it’s likely that you haven’t reached your peak earning potential yet. This means that your current tax bracket is probably lower than what it might be towards the end of your career. In this situation, a Roth IRA would make the most sense¹.

On the other hand, if you expect to be in a lower tax bracket when you start making withdrawals compared to when you were contributing, a Traditional IRA could be a better fit for you¹. - Investment Options: IRAs typically offer a wide range of investment options, including stocks, bonds, mutual funds, and ETFs. This extensive selection allows you to diversify your portfolio and choose investments that align with your risk tolerance and financial goals. If you compare it with your employer-sponsored 401k plan the selection of investment assets is often broader, which for the reasons mentioned above is to your benefit.

- No Employer Sponsorship Required: Unlike 401(k)s, which are tied to your employer, anyone with earned income can open an IRA. This offers flexibility for those who are self-employed, between jobs, or who want to save for retirement outside of their work plan.

The Not-So-Good Stuff about IRAs:

- Early Withdrawal Penalties: If you withdraw funds from an IRA before age 59.5, you may have to pay a 10% early withdrawal penalty in addition to income taxes. With a Traditional IRA you’ll have to pay taxes on both contributions and earnings because the account was funded with pre-tax dollars. With a Roth IRA you can withdraw the contributions you made (the money you put in) at any time without paying tax or a penalty. However, if you withdraw earnings (the profit you made from the money you put in) early, you may have to pay income tax and a 10% penalty. There are some exceptions to this rule for certain qualifying expenses, but in general, it’s best to leave the money in your account until retirement².

- Contribution Limits: There are annual limits on the amount you can contribute to an IRA. For 2024, the limit is $7,000, or $8,000 if you’re age 50 or older. This limit applies to all your IRAs combined, so if you have multiple IRAs, you’ll need to ensure your total contributions don’t exceed the limit³.

- Income Restrictions: For Roth IRAs, there are income limits that determine whether you can contribute. If your income is too high, you may be limited in how much you can contribute, or you may not be able to contribute to a Roth IRA at all. However, there are no income limits for Traditional IRAs. For additional information on the imposed limits and how they may affect your specific situation, please visit the IRS website.

Keep your retirement investments Halal by choosing the right partner

So, there you have it! The good and bad about IRAs in a nutshell. If your long-term financial goal is saving up for retirement, then the IRA should be your vehicle of choice. The investments you choose to bring along for the ride is something we can help out with in order to keep your IRA halal. At Wahed, our goal is to provide the gold standard in halal investing and Riba-free financial alternatives for Muslim investors. We uphold this standard by offering our clients globally diversified portfolios that are uniquely tailored to their situation and financial goals. We ensure that our investments are strictly Shar’iah by rigorously screening everything through our Shar’iah Supervisory Board, so that you can rest assured that your investments and returns are Halal.

To learn more about how Wahed can help you achieve your retirement goals visit the following page for more details.

Disclaimers:

*The term 'Halal' denotes that it is permitted and follows Islamic law

*For more information on IRA accounts please visit IRS.gov

*Consult with your tax or financial advisor before implementing any plan changes as your situations may vary.

Sources:

- Early Withdrawal Penalties for Traditional and Roth IRAs (investopedia.com)

- Last-Minute IRA Contributions Might Lower Your Taxes - https://www.forbes.com/advisor/retirement/last-minute-ira-contributions/

- 401(k) limit increases to $23,000 for 2024, IRA limit rises to $7,000 | Internal Revenue Service (irs.gov)

Risk Warning: Equity investments are not readily realisable and involve risks, including loss of capital, illiquidity, lack of dividends and dilution, and it should be done only as part of a diversified portfolio. Investments of this type are only for investors who understand these risks. You will only be able to invest in the company once you have met our conditions for becoming a registered member.

Please visit www.wahed.com/uk/ventures/risk for our full risk warning.

Risk Warning: As with any investment, a Wahed Invest Ltd investment puts your money at risk, as the value of your investment can go down as well as up. The tax treatment of your investment will depend on your individual circumstances and may change in the future. If you are unsure about whether investing is right for you, please seek expert financial advice.

Please visit www.wahed.com for our full terms and conditions

Maydan Capital Limited, trading as WahedX, is registered in England and Wales (Company No. 13451691), registered office: 87-89 Baker Street, London, W1U 6RJ, UK. Maydan Capital Ltd (FRN: 963613) is an appointed representative of Wahed Invest Ltd (FRN: 833225), an authorised and regulated firm by the Financial Conduct Authority.Wahed Invest Ltd. is registered in England and Wales (Company No. 10829012), registered office: 87-89 Baker Street, London, W1U 6RJ, UK and is authorised and regulated by the Financial Conduct Authority: FRN 833225.

Subscribe For More Islamic Finance Content

As with any investment, a Wahed Invest Ltd investment puts your money at risk, as the value of your investment can go down as well as up. The tax treatment of your investment will depend on your individual circumstances and may change in the future. If you are unsure about whether investing is right for you, please seek expert financial advice.

Wahed Invest LLC (Wahed) is a US Securities and Exchange Commission (SEC) registered investment advisor. Wahed Invest provides brokerage services to its clients through its brokerage partner Apex Clearing Corporation, a member of NYSE - FINRA - SIPC and regulated by the SEC and the Commodity Futures Trading Commission. Registration does not imply a certain level of skill or training. Wahed does not intend to offer or solicit anyone to buy or sell securities in jurisdictions where Wahed is not registered or a region where an investment practice like this would be contrary to the laws or regulations. Any returns generated in the past do not guarantee future returns. All securities involve some risk and may result in loss. Any performance displayed in the advertisements or graphics on this site are for illustrative performances only.

Disclaimer: Wahed Technologies Sdn Bhd ("Wahed") is a Digital Investment Manager (DIM) licensee issued by Securities Commission Malaysia (eCMSL/ A0359/2019). It is part of Wahed Inc. Wahed is authorized to conduct a fund management business that incorporates innovative technologies into automated portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007. All investments involve risks, including the possibility of losing the money you invest, and the track record does not guarantee future performance. The history of returns, expected returns, and probability projections is provided for informational and illustrative purposes, and may not reflect actual future performance. Wahed is not responsible for liability for your trading and investment decisions. It should not be assumed that the methods, techniques, or indicators presented in this product will be profitable, or will not result in losses. The previous results of any trading system published by Wahed, through the Website or otherwise, do not indicate future returns by that system, and do not indicate future returns that will be realized by you.

Wahed Limited - Nigeria: All investments involve risks, including the possibility of losing the money you invest, and the track record does not guarantee future performance. The historical returns and expected returns is provided for informational and illustrative purposes, and may not reflect actual future performance. Wahed is not responsible for any losses arising from your trading and investment decisions. It should not be assumed that the methods, techniques, or indicators presented in this product will be profitable, or will not result in losses. The previous results of any trading system published by Wahed, through the Website or otherwise, do not indicate future returns by that system and do not indicate future returns that will be realized by you. Wahed Limited (Wahed) is registered and regulated by the Securities and Exchange Commission, Nigeria. Wahed Limited is a subsidiary of Wahed Inc. Please visit www.wahed.com for full terms and conditions.

Wahed Invest Limited is regulated by ADGM’s Financial Services Regulatory Authority (“FSRA”) as an Islamic Financial Business with Financial Services Permission for Shari’a Compliant Regulated Activities of Managing Assets and Arranging Custody [Financial Permission No. 220065]. Our ADGM Registered No. is 000004971.

Wahed assumes no obligation to provide notifications of changes in any factors that could affect the information provided. This information should not be relied upon by the reader as research or investment advice regarding any issuer or security in particular. Any strategies discussed are strictly for illustrative and educational purposes and should not be construed as a recommendation to purchase or sell, or an offer to sell or a solicitation of an offer to buy any security. Furthermore, the information presented may not take into consideration commissions, tax implications, or other transactional costs, which may significantly affect the economic consequences of a given strategy or investment decision. This information is not intended as a recommendation to invest in any particular asset class or strategy or as a promise of future performance.

There is no guarantee that any investment strategy will work under all market conditions or is suitable for all investors. Each investor should evaluate their ability to invest long term, especially during periods of downturn in the market. Investors should not substitute these materials for professional services and should seek advice from an independent advisor before acting on any information presented. Any links to third-party websites are provided strictly as a courtesy. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites. When you access one of these websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites.